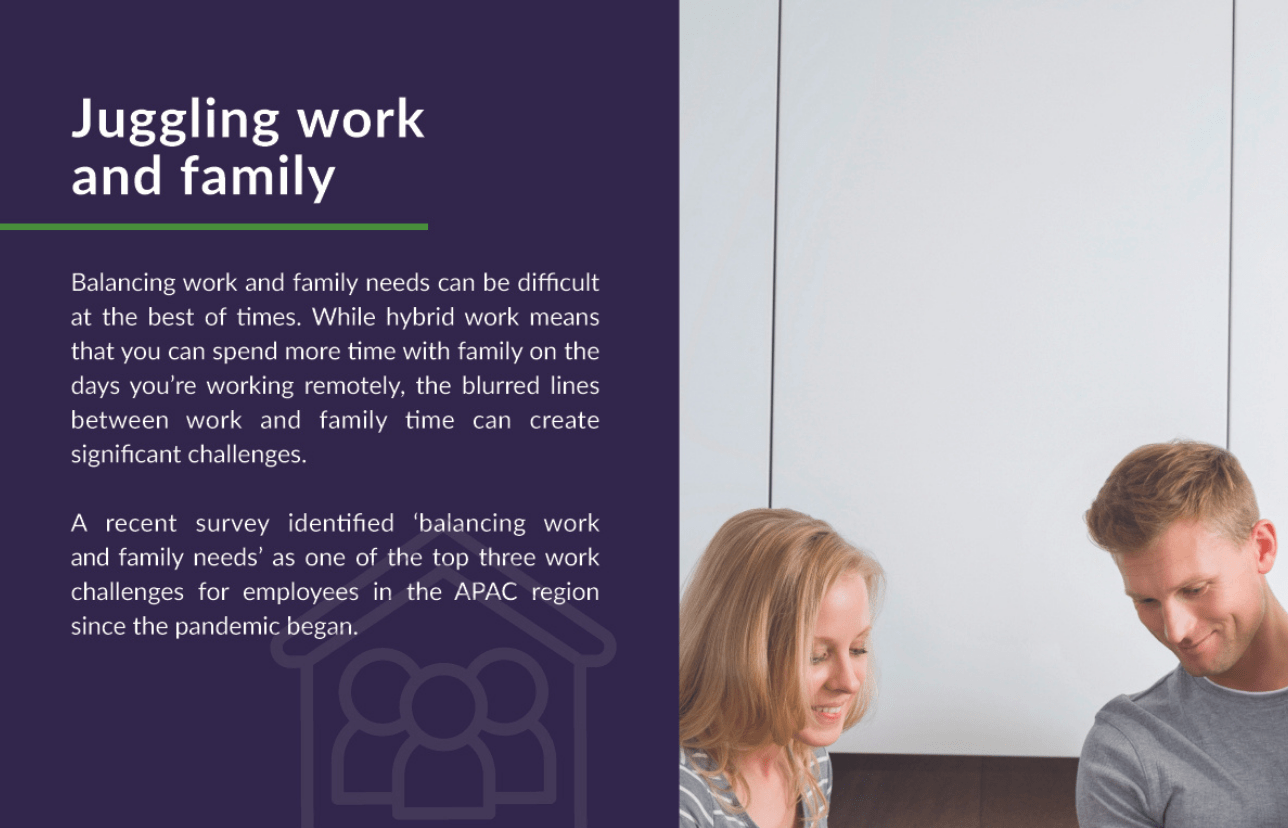

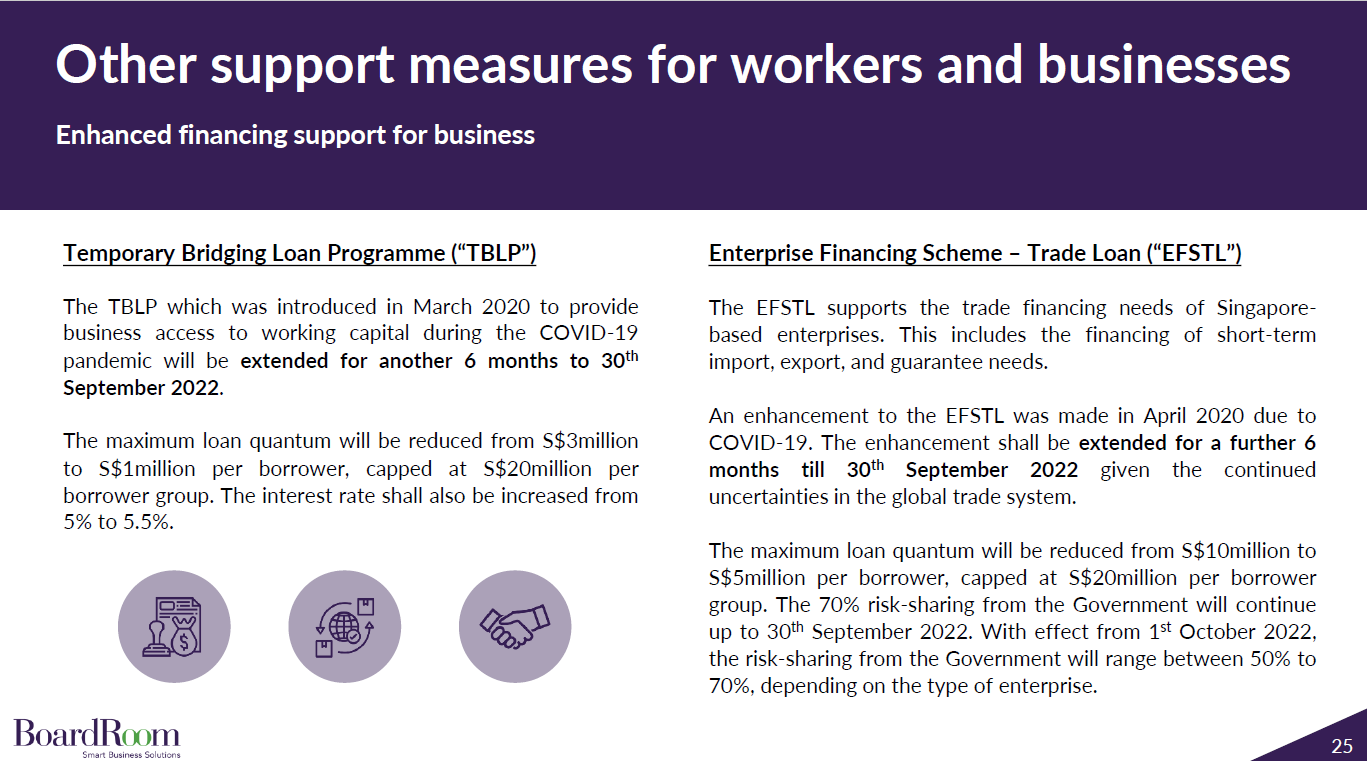

Flexible working is no longer a unique perk offered by trendy startups and technology giants. It is now a business imperative for any organisation and encompasses much more than just a remote work lifestyle. Companies that ignore people’s wishes for flexible working arrangements, including flexible leave and benefits, are missing out on retaining and engaging their current employees, boosting their employer brand and, ultimately, attracting top talent.

Flexible working environments are a chief concern across the Asia-Pacific region. A recent study by the Institute of Public Studies (IPS) found that 1 in 2 Singapore workers believe flexible work arrangements should be the new norm. But flexible work is now defined beyond a hybrid office environment. Employees are seeking flexibility to maintain better work-life balance, requesting flexible leave policies, benefits, and working hours.

Failing to implement flexible working arrangements may result in your top talent walking out the door. And replacing those people is becoming increasingly difficult. Over half of Chief Human Resources Officers (CHROs) reported the shortage of critical talent as the No.1 trend impacting organisations. HR experts warn that businesses that refuse to offer flexible work options could be losing out on up to 70% of job seekers.

Changing your policies overnight to accommodate flexible work, however, isn’t easy. We’ve put together our top tips to help you identify how flexible benefits might work in your organisation and how to create a positive work-life balance for your employees.

What is the meaning of flexible working?

By definition, flexible working is a shift away from traditional working models to adopting more versatile arrangements, such as staggered working hours and the option to work remotely. Most organisations acknowledge the importance of work-life balance and have been practising flexible work arrangements for some time. Things like part-time hours, job sharing, and time in lieu all constitute flexible working.

Post-pandemic, a common example of flexible working in Singapore is a split or hybrid work week. This is when people spend two days in the office and three days at home (or some such combination). Flexible working hours are also more common nowadays, where employees have the option to come into the office between a specified time bracket and leave after they have completed their necessary time in accordance with when they came in.

But flexible working can also be presented in other ways, and your employees are searching for solutions to help improve their work life balance.

What are the benefits of flexible working?

The benefits of flexible working are wide-ranging for employers and employees alike.

Some benefits for both parties include:

- Work/Life Balance: With the option to manage their own time effectively, employees can balance their personal commitments with their work duties, providing them more time to focus on the things they enjoy or need to take care of outside of work. This could involve attending gym classes, picking up their kids from school, and so on.

- Employee Retention and Satisfaction: When presented with flexible options when it comes to work, employees feel more respected and understood by their employers, which translates to increased loyalty and commitment.

- Productivity and Motivation: Flexible working allows team members to tackle their tasks more effectively, where they have the choice to work from environments they are more comfortable in or at times when they are most productive.

- Alleviated Stress: Employees are less likely to experience burnout or feel high levels of stress if they are allowed to work more flexibly.

- Autonomy: Many employees fail to work well under pressure or when they feel as if they are being micromanaged. Flexible working allows for a level of autonomy where employees can manage their own work and feel trusted by their employers to get the job done.

- Successful Recruitment: Potential candidates in the modern workforce are more likely to accept a job offer if the package includes flexible working options, such as hours or remote working benefits.

What are some examples of flexible working?

Flexible working hours

Allowing employees to stagger start and finish times to suit their schedules can make a big difference to their workstyle and efficiency. This gives staff an opportunity to work at a time that best suits their lifestyle, providing it doesn’t impact productivity. If you decide to offer flex time, it might be best to allocate a few hours during the week where all employees should be online simultaneously, or schedule a regular check-in so everyone is on the same page.

Medical leave without certification

This can be a fairly simple change with a significant effect. Not asking for medical certification when employees are sick helps build trust, and shows flexibility and understanding from the employer.

Condensed schedules

This could be anything from a four-day workweek to a nine-day fortnight. Allowing staff to work fewer hours can promote greater productivity. It gives your employees a chance to improve their work-life balance and also helps the business financially.

Unlimited leave

Offering employees unlimited leave is a trend with technology giants Netflix, Adobe and Hubspot. They offer unlimited paid time off (within certain parameters) to align with their strong employee-focused policies. While this is not sustainable for most companies, you may like to adopt a flexible leave approach that works for your business. It is important to note that most employees will not take advantage of this policy, and they will feel higher levels of appreciation towards the company and use their leave respectfully in turn.

Birthday leave

Everyone loves a day off for their birthday, so why not offer it as an extra paid day off for all employees? This small cost to the business could be the deciding factor in recruiting and retaining skilled employees. It sends a clear message that the company supports and actively promotes your health and wellbeing.

FLEXCATIONS & WORK TRAVEL

Giving your staff the opportunity to combine work with personal travel allows them to maximise their vacation time without it impacting work schedules. An example of this could be an employee traveling to their holiday destination on a Thursday night, working remotely on Friday and then starting their holiday at 5pm that day. In doing so, the employee can maximise their time away without any impact to their productivity.

Temporary changes in schedules

Allowing employees to make temporary changes to their office hours, reducing to part-time for a short period or taking on more hours when needed, gives them the flexibility to work around personal or family commitments while still staying loyal to the organisation.

Lifestyle or recreation leave

Granting employees leave to pursue interests or activities that are important to their wellbeing. This might include sporting activities, volunteering opportunities or health and wellness activities.

BUILD A FLEXIBLE WORKING/BENEFITS POLICY THAT WORKS FOR YOUR ORGANISATION

Understanding the many different ways to apply flexible opportunities will help you foster a strong sense of company loyalty and respect. Empowering your leaders to deliver these flexible benefits builds rapport and strengthens connections amongst teams.

With greater flexibility comes greater loyalty

Despite an overwhelming push from workers to offer more flexibility, some organisations are still resisting. A study by Ernst & Young revealed that 35% of employers want all of their employees to return to the office full-time post-pandemic.

Fears around lack of oversight, impact on collaboration efforts and challenges in making flexibility equal for everyone make it difficult for some to embrace flexibility in the workplace. But starting small is better than no start at all. Take a look at what simple changes you can implement and let your employees guide you in building a flexible workplace model that works for them.

Improving employee wellbeing and building trust

Beyond the benefits of increased retention, job satisfaction and worker engagement, perhaps the biggest payoff for organisations offering flexibility is building trust.

Trusting your staff to work when they say they will is one of the most empowering things you can do for your people. Without the constant supervision of their bosses, people feel more in control, more autonomous and empowered.

In offering flexible leave and benefits, employers can not only show their loyalty and appreciation to current employees, but also appeal to new candidates, widening your recruitment pool.

How to introduce flexible working into your organisation

Before you research all the ways you can offer flexibility, it’s important to step back and consider the basics.

Understand what flexibility means for your company and team

Just as your organisational and employee values need to be fundamentally aligned, so do your flexible working arrangements. Without understanding what flexibility means for your people and how they want to shape it, you may be creating ‘benefits’ that people aren’t interested in taking up. Or, worse still, you may create the illusion of bias by offering flexibility to some but not others.

You can use engagement and pulse surveys to uncover the key issues around flexibility for your people. What are they struggling with? What would make the biggest difference to them right now? And how do they view flexibility at work in their own roles?

It’s also important to consider generational differences, particularly if your organisation is demographically diverse. Given that most companies now have as many as five generations of workers, it’s likely that everyone’s ideas around flexibility and what is beneficial for them are going to differ. Flexibility to someone in their 20s is unlikely to mean the same thing as it does for someone in their 60s.

How do flexible benefits work?

One way that organisations are tackling this issue is with flexible benefits. Here’s a quick rundown of how flexible benefits work.

Offering these types of flexible benefits can be a good way to ensure people are getting value from the benefits you’re offering.

It’s important to note that in Singapore, organisations that want to offer flexible benefits must ensure they are correctly reflecting the value of the benefits in Central Provident Fund (CPF) payments. It may be worth getting the help of a trusted HR and payroll advisor with knowledge of the local regulations, as the rules are complex and can be confusing.

Assess your organisation’s readiness for flexible working

Review the purpose, mission and realities of your business. How much flexibility can you put into your essential services and what kind of flexibility makes sense for your organisation?

What will the initial impact be on your employees and how will you manage this impact? Having the answers to these questions will allow for a smoother transition and greater acceptance of flexible leave and benefits.

Some flexible benefits and leave policies might happen overnight, while others will take time. Building the right framework and gauging employee perspective and support is crucial.

It’s important to examine your current systems and ensure any new initiatives can be integrated. There may also be knock-on effects of introducing new flexible ways of working, for example, the implications of withholding tax in certain jurisdictions. It can be wise to get expert advice from a trusted corporate services provider.

Look at business contingency plans and practical implementation methods

Having a robust strategy and contingency plan for any flexible work arrangement is essential. It’s important to mitigate any risk to both employees and the company when any new framework is implemented.

Work with your leaders to ensure work can continue seamlessly. What processes do you need to put in place to minimise disruption?

Consider hiring an external expert who can advise on implementing flexible policies. They can help review the complexities with the leadership team and ensure executive alignment to advise on possible solutions.

As always, consistent communication about the purpose and practicalities of flexible work is key. Sometimes the biggest hurdle is the last hurdle, which is often communicating why you’re doing what you’re doing. Although with flexible working, and the many benefits it offers, this shouldn’t be too difficult, provided you’ve taken the time to really understand what flexibility means to your employees.

Take small steps to a build a more flexible workplace

Flexible working isn’t just a pandemic-related side effect — it will fundamentally shape how we work in the future. And in many ways, it already has. Singaporean organisations that take notice of it and implement flexible working arrangements now, such as working hours and flexible leave policies, will benefit from better retention rates, more engaged and productive employees, and a stronger employer brand.

But don’t be tempted to implement a blanket policy or copy a model from another organisation.

It’s important to create the right type of flexibility for your organisation. Find out what flexibility means to your people, consider your business needs and find a solution that works for your company.

Remember, you can start small when introducing flexibility into your workplace.

It doesn’t have to be a bold shift. You can introduce flexibility in incremental phases or start with small initiatives. These initiatives might include closing the office at 4pm on a Friday or giving someone the day off on their birthday. Sometimes the smallest gestures can have the biggest impact on your people.

What does flexible working look like in your organisation now and where would you like to be?

Enhance productivity and employee satisfaction

To implement flexible working arrangements with minimal disruption to current operations, one approach is to improve the efficiency of existing workflows and reduce manual labor hours. BoardRoom’s team of experts help to take the stress off your HR team by optimising your payroll processing, which reduces payroll error and in turn employee dissatisfaction. Reach out to us to discuss how you can benefit from our experienced payroll specialists.

Related Business Insights

-

05 Apr 2024

What Are the Key Benefits of Outsourcing Accounting Services?

Explore the advantages of engaging BoardRoom’s accountancy services, a leading accounting firm offering tailored …

READ MORE -

05 Apr 2024

What Factors Should Businesses Consider When Choosing the Right Accounting Firm?

Explore key factors for choosing the right accounting firm. Partner with BoardRoom for the best financial managemen …

READ MORE -

22 Mar 2024

ESG Reporting Essentials – Your Guide to ESG Reporting in Singapore

Boost transparency and build trust with comprehensive sustainability tracking and ESG reporting solutions. …

READ MORE